Managing company spending is a balancing act between cash flow control and cost. Credit cards have traditionally provided businesses with a convenient way to pay vendors and employees, but they come with significant fees and debt risk. Recent government and Reserve Bank of Australia (RBA) proposals to remove card surcharges and reduce interchange fees highlight the rising cost of credit card acceptance. This article compares business debit and credit cards from the perspective of cash flow and costs and explains why debit cards have become the smarter choice for Australian SMEs.

Cost differences

Fees borne by merchants

Merchant service fees combine interchange fees (paid to card issuers) and scheme fees (paid to card networks). In 2025, the RBA proposed caps on interchange fees: debit transactions would be capped at 0.2 % of the transaction value for card‑present transactions and 1.15 % for card‑not‑present transactions, while credit transactions would be capped at 0.4 % and 1.5 % respectively . Domestic payment costs often reflect these differences. According to Canstar, the average cost of accepting a Visa or Mastercard debit card is roughly 0.5–1 %, while a Visa or Mastercard credit card costs about 1–1.5 %, and Eftpos transactions cost less than 0.5 % .

These differences matter because the government plans to eliminate card surcharges. In late 2024, the Australian Government announced its intention to ban surcharges on debit cards from January 2026, and the RBA’s July 2025 consultation proposed removing surcharging on Eftpos, Visa and Mastercard cards entirely. If surcharges are banned, merchants will have to absorb card acceptance costs, making lower‑fee payment methods more attractive.

Fees borne by cardholders

Credit cards are expensive for businesses and employees: typical features include annual fees between $150 and $1,750 per card, and interest rates around 20 % per annum. Businesses may be required to offer a personal guarantee, meaning the owner is personally liable for debt. Missed payments incur penalties, and interest accrues quickly, eroding working capital.

Debit cards avoid these costs. Because spending is limited to preloaded funds or the business bank balance, there are no interest charges or revolving debt. Budgetly’s business debit card blog emphasises that debit cards eliminate credit risk, allow businesses to spend only what they have and do not require a credit check . By avoiding interest and late fees, debit cards support healthier cash flow.

Cash‑flow considerations

The core difference between debit and credit cards is how they impact cash flow:

Aspect Debit cards Credit cards Funding source Spends money already in the business account or on a prepaid balance; no debt is created . Provides short‑term credit; debt accumulates until the statement is paid, often attracting high interest if not cleared. Visibility and control Real‑time transaction records and pre‑set spending limits mean managers can monitor expenses instantly and prevent overspending . Typically, only monthly statements are available; it is harder to track individual employee spend before the cycle ends . Risk of overspending Low – cards stop working once the balance is exhausted. Budgetly’s prepaid cards allow custom budgets and automatic resets, which reduce expense fraud and overspending . High – credit limits may encourage spending beyond budget. Misuse can lead to penalties and interest charges . Approval process Fast issuance; no credit check; virtual cards can be generated instantly . Requires credit assessment; approval can be lengthy and may need personal guarantees . Cash‑flow impact Funds leave the account at the time of purchase, promoting accurate cash forecasting. Businesses can only spend available cash, which enforces budget discipline . Spending now reduces cash later; if statements are paid monthly, it can create a false sense of liquidity and lead to surprises when large payments fall due.

Regulatory backdrop

Government proposals

In October 2024, Treasurer Jim Chalmers announced that the government was prepared to ban surcharges on debit card payments from 1 January 2026, subject to the RBA’s review . A subsequent November 2024 media release confirmed that surcharges on debit card payments collected by the Australian Taxation Office and Services Australia would cease from 1 January 2025 and that the government intended to legislate a broader ban on debit card surcharges in 2026 . The rationale was that consumers “shouldn’t be punished for using cards” and small businesses should not pay hefty fees .

RBA consultation (July 2025)

The RBA’s Merchant Card Payment Costs and Surcharging consultation paper proposed:

- Removing surcharging on Eftpos, Visa and Mastercard debit and credit card payments, noting that surcharges no longer steer consumers to cheaper payment methods .

- Lowering interchange fee caps; the central bank estimated that reduced interchange fees would save businesses about A$1.2 billion annually, benefiting around 90 % of businesses, especially SMEs .

- Requiring large acquirers to publish average costs of acceptance across card types to improve transparency .

These reforms are expected to take effect from July 2026, subject to final decisions. If implemented, merchants will no longer be able to recover card costs through surcharging and will need to choose payment methods with lower acceptance costs. This environment makes debit cards and Eftpos more compelling for businesses.

Why debit cards are better for Australian SMEs in 2026

- Lower acceptance costs. Debit transactions incur lower interchange and scheme fees than credit transactions. Eftpos and debit card fees are typically 0.5 % or less , whereas credit card fees range from 1 % to 1.5 % or higher . With surcharges likely to be banned, these differences affect merchants’ profit margins directly.

- No debt or interest risk. Debit cards draw from existing funds, so there are no interest charges and no risk of accumulating debt . Credit cards, by contrast, have high interest rates and annual fees .

- Improved cash‑flow discipline. With debit cards, transactions are settled immediately, giving businesses accurate visibility of cash outflows. This reduces the risk of budget overruns and allows for more reliable cash‑flow forecasting .

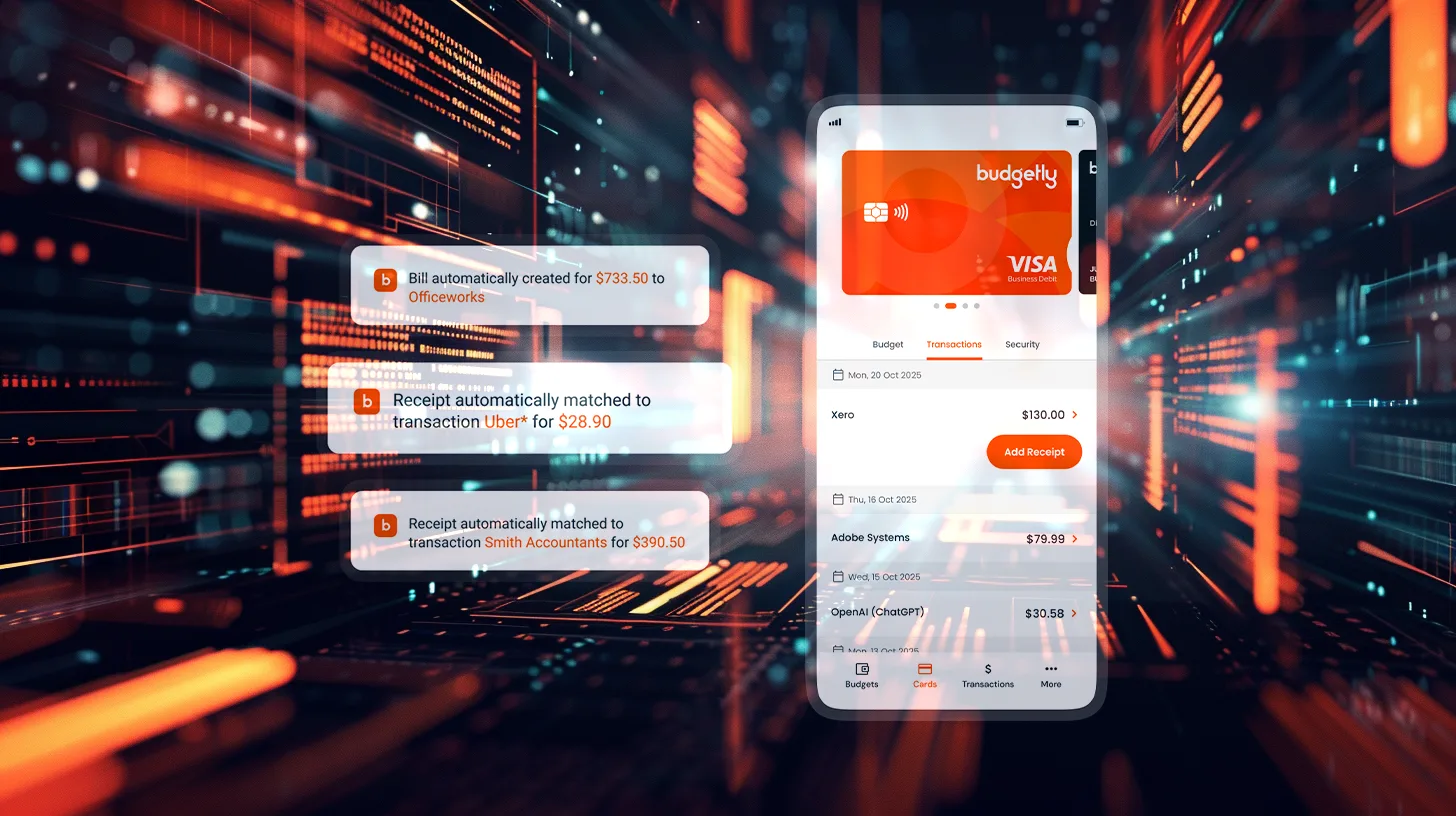

- Greater control and transparency. Modern prepaid debit cards (such as those offered by Budgetly) provide real‑time visibility, custom spending limits and automated expense categorisation. They can reduce finance‑operations costs by up to 70 % and lower the risk of expense fraud . Credit cards typically provide only monthly statements, making it harder to control spending in real time .

- Easy onboarding. Debit cards do not require a credit assessment or personal guarantee; they can be issued quickly and even virtually . Credit cards often require a formal application and can expose business owners to personal liability .

Implementing a debit‑first policy

For SMEs looking to adopt debit cards over credit cards, the following framework can help:

- Analyse current payment costs. Review merchant statements to identify average cost of acceptance for each payment method. Use the RBA’s proposed interchange caps (0.2 % for debit; 0.4 % for credit for card‑present transactions ) and Canstar’s typical ranges (Eftpos <0.5 %, debit 0.5–1 %, credit 1–1.5 % ) to benchmark your costs.

- Assess cash‑flow patterns. Determine whether delayed payment cycles from credit cards create budgeting surprises. Evaluate whether immediate settlement via debit cards would provide more accurate visibility and reduce risk.

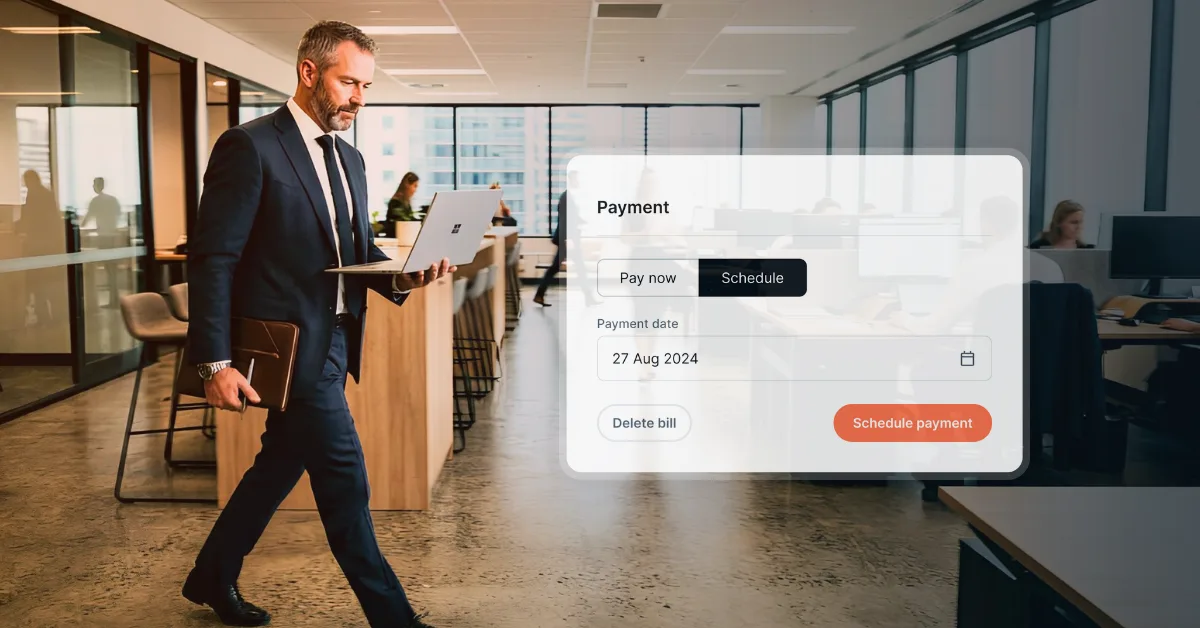

- Evaluate control requirements. Decide which teams or employees require card access. Debit cards with pre‑set limits, approval workflows and real‑time notifications can prevent overspending and simplify reconciliation .

- Choose a provider with robust software. Look for platforms that integrate with accounting software (e.g., Xero), support automated receipt capture, and offer customisable budgets. Budgetly’s prepaid corporate cards, for example, deliver real‑time tracking, custom spending rules and automated reporting .

- Prepare for regulatory changes. As surcharging bans take effect in 2026, update pricing and budgeting strategies to absorb card costs. Opting for low‑cost payment methods like debit cards will minimise margin impact.

Conclusion

Rising merchant fees and impending surcharging bans make it imperative for Australian SMEs to rethink their payment strategies. Credit cards come with high costs, annual fees, interest rates, and higher merchant fees, and can create cash‑flow distortions. Debit cards, particularly prepaid corporate cards, offer a lower‑cost, debt‑free alternative that improves financial control and transparency. With government reforms favouring low‑cost payment methods, a debit‑first strategy positions businesses to protect margins and manage cash more effectively.

Would you like to (a) explore debit card solutions like Budgetly in more detail, (b) compare integrated spend‑management platforms, or (c) discuss other cash‑flow improvement strategies?