Bookkeeping is one of the most critical foundations of business finance, yet it’s also one of the most overlooked. For CFOs, bookkeepers, or finance leads, getting the basics right ensures your records are compliant, your cash flow is healthy, and your business can grow with confidence.

In this guide, we’ll cover the fundamentals of bookkeeping: what it is, why it matters, and how you can manage it efficiently with modern tools and processes.

- What is bookkeeping?

- What does a bookkeeper do?

- Why bookkeeping is important

- When to set up bookkeeping in your business

- Types of bookkeeping systems

- Key reports to track

- Benefits of good bookkeeping practices

- Common mistakes to avoid

- How Budgetly supports smarter bookkeeping

- Lay the groundwork for confident financial decisions

What is bookkeeping?

Bookkeeping is the process of recording and organising a business’s financial transactions. It includes income, expenses, purchases, payments, and everything in between.

What does a bookkeeper do?

A bookkeeper maintains accurate records of financial activity. Their responsibilities typically include:

- Tracking daily transactions

- Reconciling bank statements

- Preparing financial reports

- Managing payroll entries and receipts

- Ensuring compliance with ATO requirements

## Why bookkeeping is important

Good bookkeeping is about more than just tax, it helps you:

- Monitor business performance

- Maintain accurate cash flow

- Make confident financial decisions

- Keep your business audit-ready

When to set up bookkeeping in your business

You should have bookkeeping systems in place as soon as your business starts generating income. Even if you’re not registered for GST yet, keeping proper records ensures you’re ready for growth, investment, or compliance audits.

Types of bookkeeping systems

Choosing the right bookkeeping system depends on your business size, transaction volume, and in-house expertise. There are three main types:

- Manual bookkeeping: This involves recording transactions by hand using ledgers, notebooks, or spreadsheets. While it’s inexpensive and straightforward, it’s prone to human error and becomes difficult to manage as your business scales.

- Software-based bookkeeping: Accounting software like Xero, MYOB, or QuickBooks offers more robust tools for managing income, expenses, and reporting. These platforms automate many tasks like bank reconciliations and GST tracking, making them ideal for businesses with moderate to high volumes of transactions.

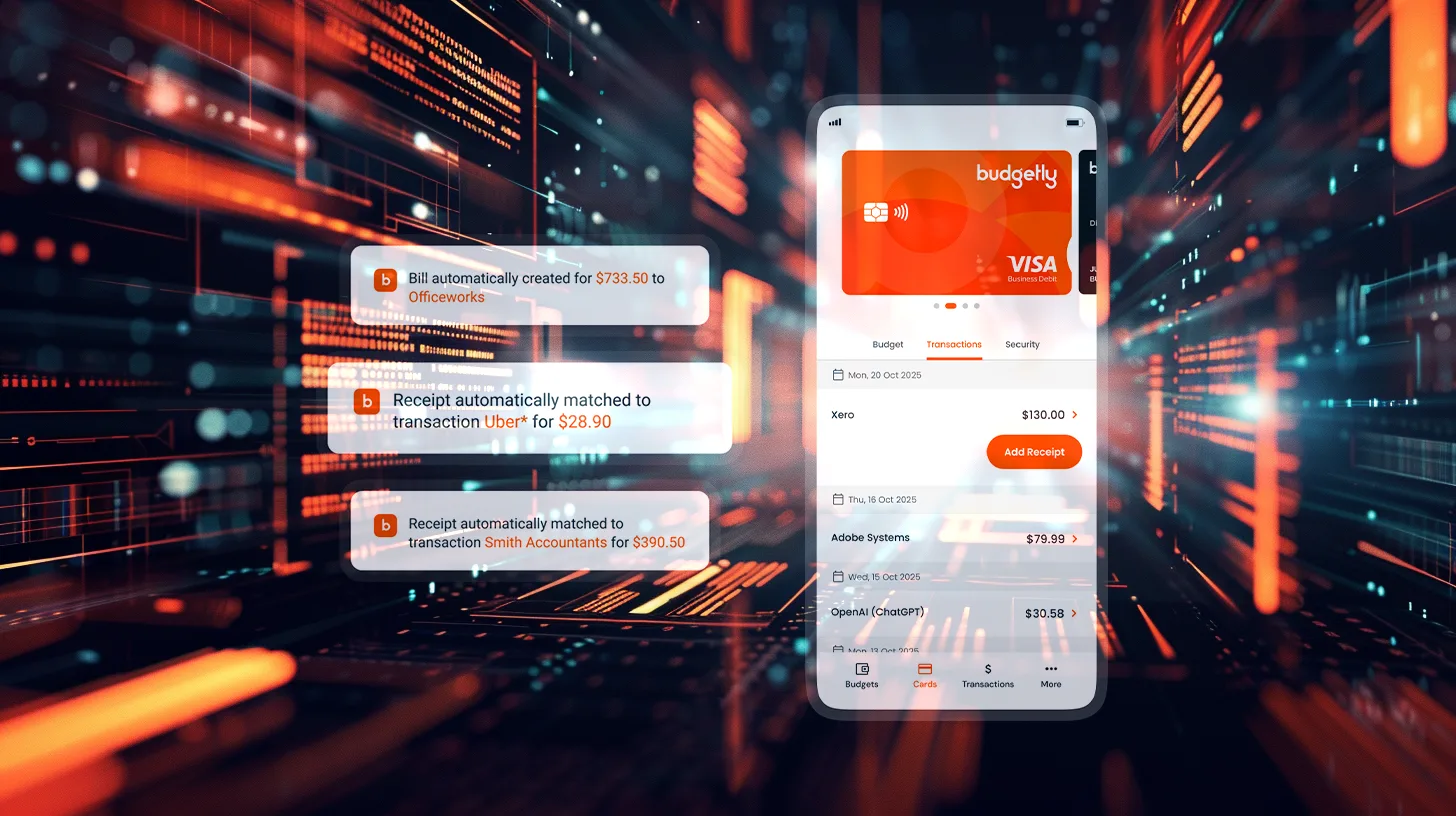

- Cloud-based bookkeeping with add-ons: Businesses increasingly adopt connected ecosystems by combining accounting software with supporting tools. For example, using budget management software like Budgetly helps finance teams manage real-time spending, track receipts, and automate expense categorisation. These integrations reduce manual work, improve accuracy, and allow you to focus on financial decision-making.

Key reports to track

Keeping an eye on core financial reports ensures you understand how your business is performing and where adjustments may be needed:

- Profit and loss statement (P&L): Summarises revenue and expenses over a set period. It shows whether your business is generating a profit or operating at a loss.

- Balance sheet: Provides a snapshot of assets, liabilities, and equity at a specific point in time. It’s essential for understanding your company’s financial position.

- Cash flow statement: Tracks the flow of money in and out of the business. It highlights whether your operations generate enough cash to meet obligations.

- Accounts receivable and payable reports: Help track who owes you money and who you owe. Timely follow-ups can improve cash flow and vendor relationships.

- General ledger: A complete record of all financial transactions categorised by accounts. It forms the basis for all your financial reporting and audits.

Finance professionals should review these reports regularly, not just at end-of-year, to make informed decisions and flag issues early.

Benefits of good bookkeeping practices

Well-maintained books benefit more than just tax time, they influence everything from funding applications to long-term planning. Here are the key advantages:

- Improved accuracy: Clean, up-to-date records reduce the risk of errors and make it easier to detect inconsistencies early.

- Faster tax preparation: Organised transactions and clear documentation simplify BAS and end-of-year tax returns, reducing reliance on last-minute scrambling.

- Better budgeting and forecasting: Historical data gives you the insight needed to plan effectively for growth or respond to financial challenges.

- Increased funding opportunities: Lenders and investors often request financial records. A strong bookkeeping history builds trust and increases your eligibility.

- Audit-readiness: Good records minimise the stress and workload involved in preparing for ATO reviews or external audits.

In short, bookkeeping is a safeguard, and an enabler, for smarter, more confident business management.

Common mistakes to avoid

Even with the best intentions, finance teams can fall into habits that lead to inaccurate records and wasted time. Avoid these common pitfalls:

- Mixing business and personal expenses: This makes it harder to categorise transactions correctly and can cause legal and tax issues. Use dedicated corporate cards or corporate prepaid cards to separate business spending.

- Delaying data entry: Letting weeks go by without recording transactions increases the chance of errors, duplicates, or missing receipts.

- Not backing up financial records: If you’re using desktop-based systems or paper records, you risk losing critical data. Cloud storage and real-time syncing tools can mitigate this.

- Incorrectly categorising expenses: Misclassifying a purchase (e.g., capital vs operational expenditure) can affect your financial reports and tax deductions.

- Overlooking GST documentation: Without valid tax invoices and receipts, your business may lose out on claiming input tax credits, reducing your profitability.

By avoiding these mistakes, and leveraging tools to support consistency, you can keep your books accurate and audit-ready year-round.

How Budgetly supports smarter bookkeeping

Budgetly helps reduce errors at the source by ensuring your expense data is captured and categorised accurately in real time.

- Prepaid cards mean no more out-of-pocket expenses

- Receipts are uploaded and matched immediately

- Transactions are auto-categorised for accounting

- Export-ready data keeps your books clean and audit-ready

- Use Budgetly as part of your budget management software ecosystem for smarter forecasting

Lay the groundwork for confident financial decisions

Effective bookkeeping sets the tone for how your business grows, how you manage risk, and how much time you spend on admin. Whether you’re getting started or tightening up your current process, now is the time to build stronger foundations.

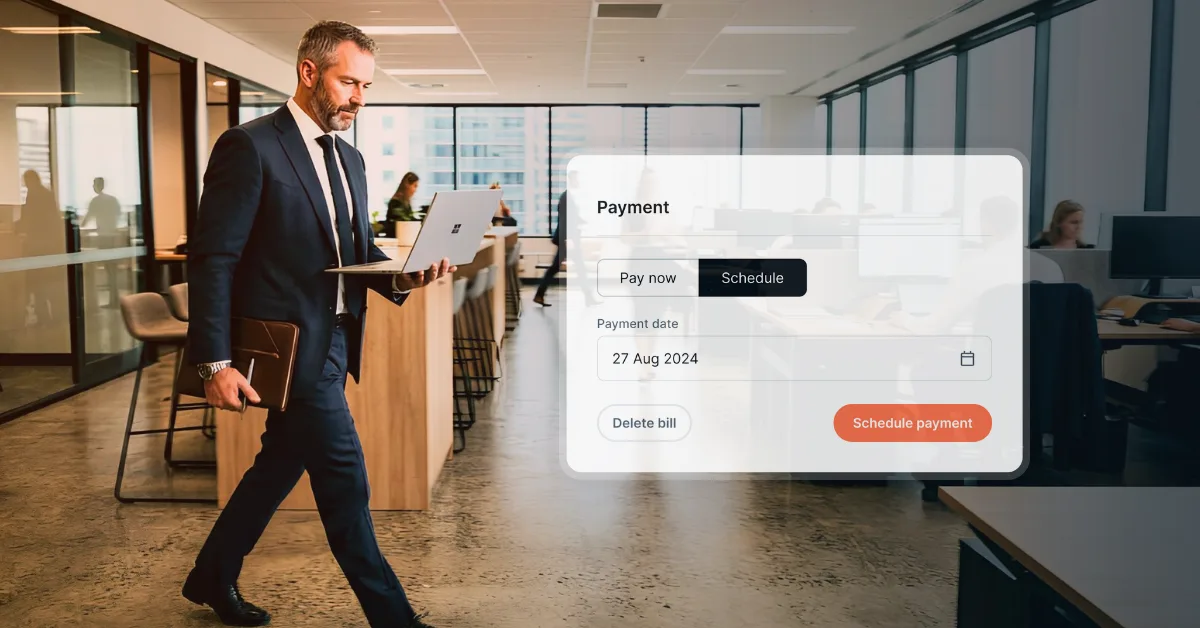

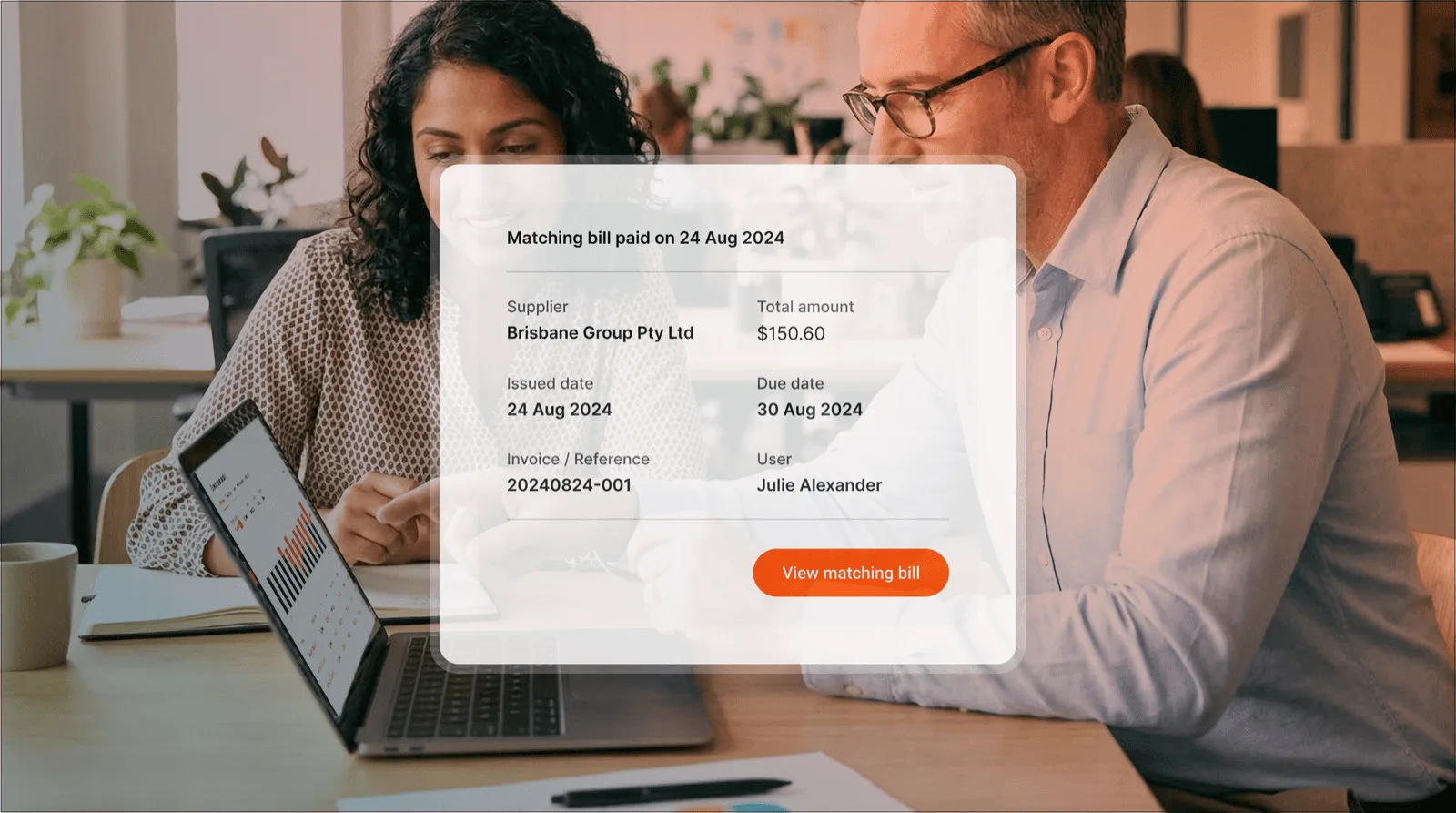

With tools like Budgetly, you can simplify manual tasks and keep your records accurate in real time. Capture every transaction using smart expense tracker tools, ensure clean data flows through your Xero integration, and keep business expenses in check with reloadable virtual cards that make reconciliation easier for everyone involved.