Budgetly’s expense management software

- Bookkeeping tracks your money in and out; it’s how you understand your business health, not just a tax-time chore.

- Australian businesses must stay compliant with GST, BAS, and ATO record-keeping rules.

- Core tasks include recording transactions, reconciling accounts, managing receipts, and maintaining proper documentation.

- Modern platforms like Budgetly automate repetitive work, giving you real-time spending insights and slashing admin time so you can focus on what actually matters: running and growing your business.

Table of Contents:

- What business bookkeeping actually means

- Why business bookkeeping matters for Australian businesses

- Key bookkeeping tasks every business must manage

- The different types of bookkeeping systems

- The business bookkeeping process: Step-by-step

- Common mistakes and how to avoid them

- Bookkeeping compliance in Australia

- Better business bookkeeping with Budgetly

- Turning bookkeeping data Into strategic decisions

- Frequently asked questions

What business bookkeeping actually means

Business bookkeeping is the systematic process of recording, organising, and tracking all financial transactions in your business. Think of it as maintaining a detailed financial diary. Every sale you make, every bill you pay, every expense you incur gets documented in a way that tells the complete story of your business’s money.

Bookkeeping also means maintaining several key records. Your income statements show profitability over time, balance sheets reveal what you own versus what you owe, and cash flow statements track the actual movement of money through your business. These aren’t just documents for tax season. They’re the instruments that help you read your business’s financial health in real-time.

For most small business owners, bookkeeping means dedicating time weekly or monthly to reconciling bank statements, invoicing clients, recording receipts, and ensuring every financial transaction has a proper home in your books. It’s the unglamorous but essential work that keeps your financial house in order.

Bookkeeping vs accounting: what’s the difference?

Bookkeeping

Accounting

Records daily transactions

Interprets financial data

Organises income and expenses

Prepares reports and forecasts

Reconciles bank accounts

Provides strategic advice

Maintains compliance records

Handles tax planning and audits

Tracks receipts and invoices

Analyses profit, cash flow, and trends

Good bookkeeping gives accountants clean data to work with. It also helps you prepare BAS statements, lodge tax returns, and track cash flow throughout the year, not just at tax time.

Why business bookkeeping matters for Australian businesses

Business bookkeeping isn’t just a legal requirement or administrative task you tick off your to-do list. It’s one of the most powerful management tools available to you, regardless of whether you’re a sole trader working from home or running a company with dozens of employees. Solid bookkeeping provides the financial intelligence that drives better decisions, protects your business from compliance issues, and ultimately determines whether your venture thrives or struggles.

Here’s why bookkeeping matters so much for Australian businesses, and what happens when you get it right (or wrong).

Crystal-clear visibility over cash flow

Cash flow is the lifeblood of any business. You might be profitable on paper, but if you don’t have cash available when bills are due, you’re in trouble. Accurate bookkeeping gives you a real-time picture of your financial position.

What good bookkeeping reveals:

- Exactly how much money is in your bank accounts right now

- Which customers owe you money, and how long have they been outstanding

- Which suppliers do you need to pay, and when are payments due

- Whether you have enough cash to cover upcoming expenses

- Seasonal patterns in your cash flow that help you plan ahead

The danger of poor visibility: Without accurate bookkeeping, you’re essentially flying blind. You might think you’re doing well because revenue is coming in, but you could be heading toward a cash crisis if you’re not tracking when money actually hits your account versus when expenses are due. Many profitable businesses have failed simply because they ran out of cash at the wrong moment.

Real-world impact: Imagine you’re considering hiring a new employee or making a significant equipment purchase. Without solid bookkeeping, you’re guessing whether you can afford it. With proper financial records, you can see your cash flow trends over the past six months, forecast your position for the next quarter, and make an informed decision based on facts rather than hope.

Stress-free tax returns and BAS preparation

Tax time in Australia doesn’t have to be a nightmare of scrambling through shoeboxes full of faded receipts and trying to remember what that $347 transaction from eight months ago was for.

How good bookkeeping makes tax easier:

- All your income and expenses are already recorded and categorised throughout the year

- Digital receipts are stored securely and linked to transactions

- GST collected and paid is tracked automatically

- Deductible expenses are clearly separated from non-deductible ones

- Your accountant can quickly prepare your return without hours of cleanup work

- BAS statements are simple to compile because your GST data is always current

The cost of poor tax preparation: When your records are disorganised, you face several problems. You’ll waste hours (or pay someone else to waste hours) reconstructing your financial year. You’ll likely miss legitimate tax deductions because you don’t have the receipts or can’t remember what purchases qualified. You risk ATO penalties if your records don’t support your claims. And the stress of rushing to meet lodgement deadlines is entirely avoidable.

Compliance peace of mind: The ATO requires you to keep records for at least five years. If you’re audited or they have questions about your return, comprehensive bookkeeping means you can quickly provide the documentation they need. No panic, no uncertainty, just facts at your fingertips.

Smarter budgeting and financial forecasting

You can’t plan for the future if you don’t understand your past. Historical financial data is the foundation for realistic budgets, accurate forecasts, and strategic planning.

What your bookkeeping data enables:

- Identifying spending patterns and trends over time

- Understanding which months are typically strong or weak for revenue

- Spotting areas where costs are creeping up unexpectedly

- Setting realistic budgets based on actual historical data, not guesswork

- Forecasting future revenue and expenses with reasonable accuracy

- Planning for major purchases or investments with confidence

- Making informed decisions about pricing, hiring, and expansion

Strategic advantage: When you review your profit and loss statement each month and compare it to previous periods, you start to understand your business at a deeper level. Which products or services actually make you money? Which clients are most profitable? Where are you spending more than expected? These insights only come from consistent, accurate bookkeeping.

Example scenario: You’re thinking about hiring someone. Looking at your books, you can see that your average monthly expenses are $15,000, revenue is averaging $28,000, and you typically have about three months of operating expenses in the bank. You can calculate exactly how much a new hire would cost (salary plus super plus on-costs) and model whether your current revenue trajectory supports it. That’s strategic decision-making based on financial reality.

Robust financial controls and fraud prevention

Bookkeeping isn’t just about recording what happened. It’s about creating a system of checks and balances that protects your business from errors, unauthorised spending, and fraud.

What proper controls provide:

- Clear audit trail showing who spent what, when, and why

- Spending limits that prevent unauthorised large purchases

- Approval workflows for expenses above certain thresholds

- Regular reconciliation that catches unusual or duplicate transactions quickly

- Separation of duties so no single person controls all financial functions

- Digital receipts and documentation that prevent expense manipulation

The fraud risk: Small business fraud is more common than many owners realise, and it often comes from trusted employees or contractors. Without proper bookkeeping controls, detecting fraud becomes nearly impossible until it’s too late. Regular reconciliation, spending monitoring, and clear documentation requirements create natural barriers that both prevent and detect fraudulent activity.

Tools like Budgetly help here: Modern expense management platforms give you real-time visibility into who’s spending what. You can set card limits, require receipt uploads, implement approval workflows, and monitor transactions as they happen. This level of control was once only available to large enterprises; now small and medium businesses can protect themselves just as effectively.

Audit-readiness and legal compliance

The ATO can audit your business at any time, and they have up to four years (longer in cases of fraud or significant errors) to review your tax affairs. Being audit-ready isn’t paranoid; it’s prudent.

What does audit-ready mean:

- Complete financial records for at least five years All claims supported by proper documentation (receipts, invoices, contracts)

- GST records that clearly show input tax credits and output tax collected

- Payroll records showing PAYG withholding, super contributions, and employee entitlements

- Asset registers tracking depreciation and disposals

- BAS statements that reconcile to your bookkeeping records

The cost of non-compliance: ATO penalties for poor record-keeping can be substantial. If you can’t substantiate your claims, they’ll disallow deductions, recalculate your tax, and potentially apply penalties and interest. In serious cases, directors can be held personally liable for company tax debts. Beyond financial penalties, the stress and time required to deal with an audit when your records are poor is significant.

Peace of mind: When your bookkeeping is solid, an ATO inquiry or audit is inconvenient but not catastrophic. You can provide the requested information quickly, answer questions confidently, and move on with your business. That peace of mind alone makes good bookkeeping worthwhile.

Better relationships with lenders and investors

If you ever want to secure a business loan, attract investors, or sell your business, financial records are the first thing anyone will ask for.

What stakeholders want to see:

- Consistent profit and loss statements showing business performance

- Balance sheets demonstrating assets, liabilities, and equity

- Cash flow statements prove that you generate sufficient operating cash

- Clean bookkeeping records that inspire confidence in your management

- Clear financial trends that support your growth story

- Professional presentation of financial data

Access to capital: Banks and investors won’t lend or invest based on your verbal assurances. They need documented proof that your business is viable, profitable, and well-managed. Poor bookkeeping can disqualify you from financing opportunities, even if your business fundamentals are sound. Good bookkeeping opens doors to capital when you need it for growth or to navigate difficult periods.

Informed business decision-making every day

The most valuable aspect of good bookkeeping is how it informs everyday business decisions. Every strategic choice you make (from pricing to hiring to expansion) should be grounded in financial reality.

Daily decisions bookkeeping supports:

- Should I offer a discount to win a particular contract?

- Can I afford to attend that interstate conference?

- Is this marketing campaign delivering a positive return?

- Should I increase inventory levels before the busy season?

- Which suppliers offer the best value?

- Are my pricing levels sustainable given my cost structure?

Confidence in decision-making: When you know your numbers, you operate with confidence. You’re not guessing whether you can afford something or whether a decision makes financial sense. You can look at your books, see the facts, and make choices backed by evidence. This reduces stress, improves outcomes, and helps you grow your business strategically rather than reactively.

Professional credibility and business maturity

How you manage your finances sends a signal about your business maturity. Professional bookkeeping practices demonstrate that you’re serious, organised, and capable of managing growth.

What good bookkeeping signals:

- Professional management and attention to detail

- Respect for legal and ethical business practices

- Preparedness for growth and scaling

- Trustworthiness to suppliers, customers, and partners

- The capability to handle larger contracts or clients

Business development advantage: Some larger clients and government contracts require proof of financial stability or professional accounting practices. Having solid bookkeeping in place can qualify you for opportunities that competitors with poor financial management can’t access.

## Key bookkeeping tasks every business must manage

Effective bookkeeping is the foundation of sound financial management. Whether you’re a sole trader or running a growing enterprise, staying on top of these core tasks will help you maintain compliance, improve cash flow, and make better strategic decisions.

1. Recording transactions

Every financial transaction must be accurately recorded in your accounting system. This creates an audit trail and ensures your financial reports reflect reality.

What to record:

- Customer invoices and sales receipts

- Supplier bills and purchase orders

- Payment transactions (incoming and outgoing)

- Refunds and credit notes

- Petty cash expenditures

- Employee expense reimbursements

- Bank fees and interest charges

- Loan repayments and financing costs

Best practices:

- Record transactions as they occur, not weeks or months later

- Use a digital expense tracking app to capture receipts in real-time, especially for employee spending

- Implement a consistent chart of accounts to categorise transactions uniformly

- Attach supporting documentation (receipts, invoices, contracts) to each entry

- Separate business and personal expenses completely

2. Bank reconciliation

Bank reconciliation is the process of matching your internal bookkeeping records against your bank statements to verify accuracy and completeness.

Why it matters:

- Catches bookkeeping errors and omissions

- Identifies duplicate entries

- Detects unauthorised or fraudulent transactions

- Reveals banking errors or unexpected fees

- Ensures your books reflect the actual available funds

How often:

- Monthly at minimum, though weekly reconciliation is ideal for businesses with high transaction volumes

- Reconcile all accounts: operating accounts, savings, credit cards, and merchant payment platforms

Common reconciliation issues:

- Outstanding checks that haven’t cleared

- Deposits in transit

- Bank fees not yet recorded

- Timing differences between when transactions are recorded and when they clear

- Electronic payments with unclear descriptions

3. Managing accounts receivable (AR)

Accounts receivable represent money customers owe you for goods or services delivered. Effective AR management directly impacts your cash flow and working capital.

Key activities:

- Issue accurate, detailed invoices promptly after delivery

- Establish clear payment terms (e.g., Net 30, Net 60)

- Track invoice aging to identify overdue payments

- Send payment reminders before and after due dates

- Follow up on late payments with a systematic collection process

- Offer multiple payment methods to make it easy for customers to pay

- Consider early payment discounts or late payment penalties

- Review customer creditworthiness for large orders

Warning signs:

- Aging receivables beyond 60-90 days

- The same customers consistently paying late

- Increasing days sales outstanding (DSO) ratio

4. Managing accounts payable (AP)

Accounts payable tracks money you owe suppliers and vendors. Strategic AP management helps you maintain good supplier relationships while optimising cash flow.

Key activities:

- Verify all incoming invoices for accuracy before recording

- Match invoices to purchase orders and delivery receipts (three-way matching)

- Schedule payments to avoid late fees while maximising cash availability

- Take advantage of early payment discounts when financially beneficial

- Maintain organised records of all supplier agreements

- Track recurring expenses and subscription services

- Negotiate favourable payment terms with key suppliers

- Monitor for duplicate invoices

Cash flow optimisation:

- Don’t pay too early (unless there’s a discount) or too late (to avoid penalties)

- Prioritise payments based on due dates, importance, and available discounts

- Forecast upcoming payment obligations to avoid cash shortfalls

5. Payroll management

If you employ staff, payroll compliance is non-negotiable. Errors can result in penalties, employee dissatisfaction, and ATO scrutiny.

What you must track:

- Gross wages and salaries

- Superannuation contributions (currently 11.5% as of July 2024, increasing to 12% by July 2025)

- PAYG (Pay As You Go) tax withholding

- Annual leave accrual and usage

- Sick leave and other entitlements

- Over time, penalty rates and allowances

- Workers’ compensation premiums

- Payroll tax (if your total Australian wages exceed the threshold, which varies by state)

Compliance requirements:

- Pay super at least quarterly (preferably monthly via clearing houses)

- Report and remit PAYG withholding to the ATO

- Issue payment summaries or enable employees to access via ATO online services

- Maintain detailed payroll records for seven years

- Lodge Single Touch Payroll (STP) reports at or before each pay day

- Ensure award compliance for minimum wages and conditions

Common pitfalls:

- Misclassifying employees as contractors

- Calculating superannuation on incorrect earnings

- Missing STP lodgment deadlines

- Failing to pay super on time (severe penalties apply)

6. Financial reporting

Regular financial reports transform raw bookkeeping data into actionable business intelligence. These reports are essential for decision-making, securing financing, and meeting stakeholder expectations.

Core financial statements:

Profit and Loss Statement (P&L or Income Statement):

- Shows revenue, expenses, and net profit over a specific period

- Reveals which products, services, or departments are most profitable

- Helps identify cost-saving opportunities

- Compare against budgets and prior periods

Balance Sheet:

- Snapshot of your business’s financial position at a specific date

- Lists assets (what you own), liabilities (what you owe), and equity (net worth)

- Indicates financial stability and solvency

- Essential for loan applications and investor presentations

Cash Flow Statement:

- Tracks actual cash moving in and out of your business

- Separates operating, investing, and financing activities

- Reveals whether you’re generating sufficient cash to sustain operations

- More important than profitability for short-term survival

Additional useful reports:

- Aged receivables and payables summaries

- Budget vs. actual comparisons

- Key performance indicators (KPIs) dashboard

- Department or project profitability reports

- Break-even analysis

Reporting frequency:

- Monthly reports for active management

- Quarterly reviews for strategic planning

- Annual reports for tax compliance and stakeholder reporting

7. Managing fixed assets and depreciation

Capital assets like equipment, vehicles, and property require special tracking for both tax and financial reporting purposes.

What to track:

- Purchase date and cost

- Useful life and depreciation method

- Current book value

- Disposal date and proceeds (if sold)

- Depreciation schedules for tax purposes

Why it matters:

- Claim legitimate tax deductions for asset depreciation

- Accurately report business net worth

- Plan for asset replacement

- Support insurance claims in case of damage or loss

8. GST compliance (if registered)

If your business is registered for GST, you must track and report goods and services tax on your business activities.

Requirements:

- Separate GST collected on sales from GST paid on purchases

- Lodge Business Activity Statements (BAS) monthly, quarterly, or annually

- Maintain tax invoices for all purchases over $82.50

- Reconcile GST accounts regularly

- Remit net GST to the ATO by the due date

- Need help understanding BAS? Read our complete guide to business activity statements.

Record-keeping:

- Keep detailed records of GST credits claimed

- Document reasons for GST-free or input-taxed sales

- Maintain evidence of mixed-use asset adjustments

9. Budgeting and forecasting

While not traditional bookkeeping, forward-looking financial management is essential for sustainable growth.

Benefits:

- Set realistic financial targets

- Allocate resources effectively

- Identify potential cash flow problems before they occur

- Measure actual performance against expectations

- Support funding applications and strategic planning

Best practices:

- Review and update budgets quarterly

- Create conservative, moderate, and optimistic scenarios

- Involve department heads in the budgeting process

- Use historical data to inform projections

- Build in contingency reserves for unexpected expenses

10. Document management and storage

Organised record-keeping saves time, reduces stress, and ensures compliance with ATO requirements.

ATO record-keeping expectations: The ATO requires Australian businesses to retain records for at least five years from when you prepared or obtained or completed the transactions they relate to (whichever is later).

Required records include:

- Sales and income records (invoices, receipts, sales journals)

- Purchase and expense records (supplier invoices, receipts, payment records)

- Tax invoices and receipt documentation

- Bank statements and credit card statements

- Payroll records (pay slips, superannuation records, PAYG summaries)

- Asset registers and depreciation schedules

- BAS and tax return documentation

- Contracts and agreements

- Loan and financing documents

Digital vs. paper records:

- Digital records are fully acceptable and often preferable

- Must be complete, accurate, and accessible when needed

- Implement regular backup systems (cloud and local)

- Ensure digital records are readable and searchable

- Maintain security and access controls

Retention periods for specific records:

- Payroll records: seven years

- Super contributions: five years

- PAYG withholding: five years

- Capital gains tax records: keep until five years after the asset is disposed of

- Depreciation schedules: keep for five years after disposal

Making bookkeeping manageable

Invest in the right tools: Modern cloud-based accounting software (Xero, MYOB, QuickBooks) automates much of the bookkeeping process, reducing errors and saving time.

Establish routines: Set aside dedicated time weekly for bookkeeping tasks rather than leaving everything until month-end or tax time.

Get professional help: Consider hiring a bookkeeper for regular data entry and reconciliation, and an accountant for strategic advice, tax planning, and compliance.

Separate business and personal: Maintain dedicated business bank accounts and credit cards to simplify record-keeping and protect your personal assets.

Stay educated: Bookkeeping requirements and tax laws change. Subscribe to ATO updates, attend workshops, or work with professionals who stay current.

The bottom line: Comprehensive bookkeeping isn’t just about compliance; it’s about giving yourself the financial clarity to make confident business decisions, identify opportunities, and build a sustainable enterprise. The time and resources you invest in getting your books right will pay dividends in reduced stress, better cash flow, and stronger business performance.

The different types of bookkeeping systems

There’s no one-size-fits-all approach to bookkeeping. The right system depends on your business size, transaction volume, and internal resources.

Manual bookkeeping

Recording transactions by hand in ledgers or notebooks. This method is inexpensive but slow, error-prone, and difficult to scale.

Spreadsheet-based bookkeeping

Using Excel or Google Sheets to track income and expenses. It’s more flexible than manual methods, but still requires significant manual input and offers limited automation.

Digital bookkeeping software

Platforms like Xero, MYOB, and QuickBooks allow you to automate bank feeds, reconcile accounts, and generate financial reports. These are the standards for most Australian SMEs.

Automated bookkeeping tools

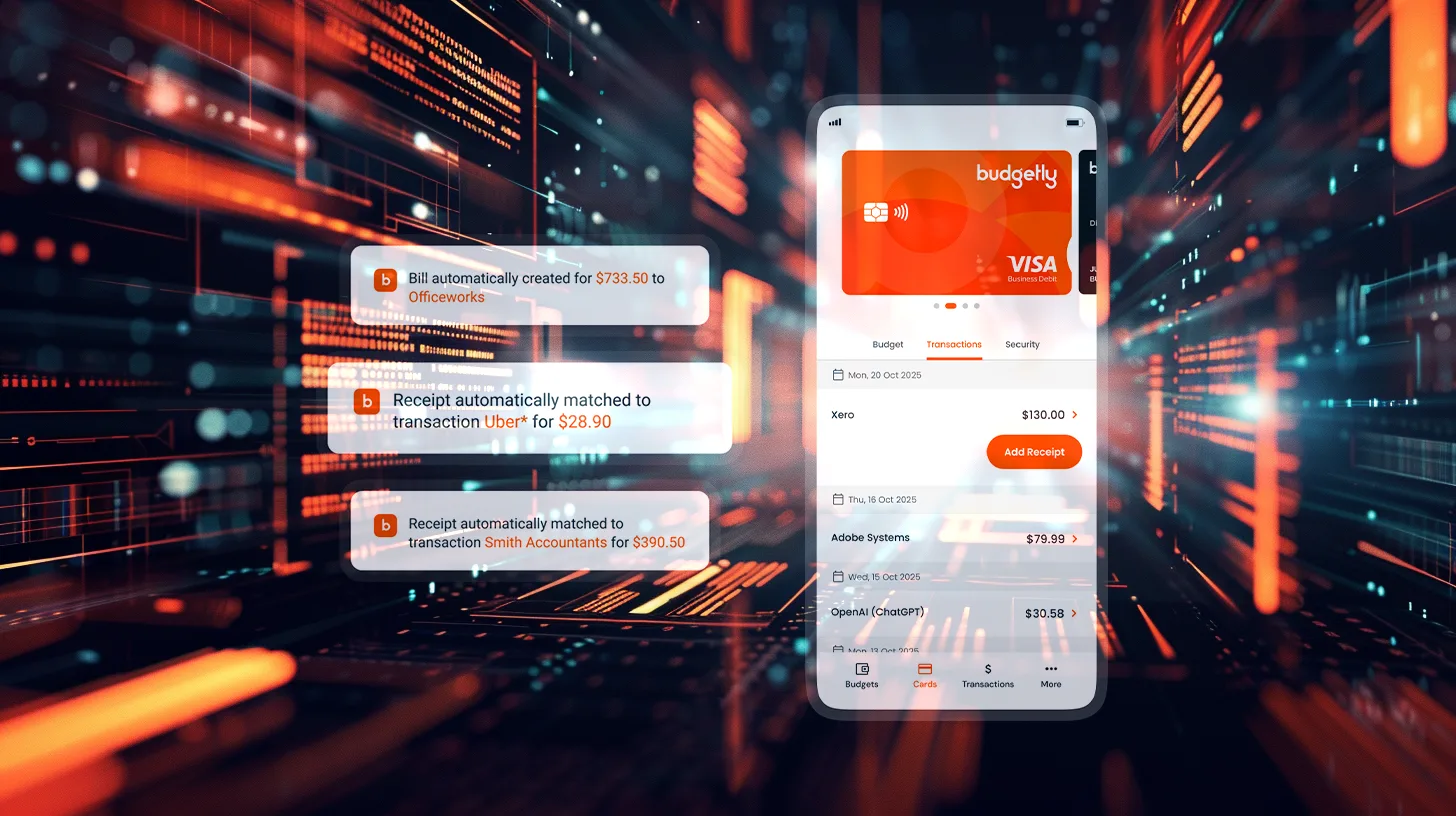

AI-powered tools can categorise transactions, match receipts, and flag anomalies. Many businesses are now using Budgetly’s expense management software to automate the expense side of bookkeeping, reducing manual data entry and improving accuracy.

Expense management platforms

These sit alongside your accounting software and focus specifically on tracking business spending. Many SMEs now issue controlled virtual business cards to staff, which automatically capture transaction data and sync it with your books in real time.

Choosing the right system depends on your needs, but in general, the more you can automate, the fewer errors you’ll make.

The business bookkeeping process: Step-by-step

Here’s a practical framework for managing business bookkeeping in your operations:

1. Set up your chart of accounts

This is a list of all the categories you’ll use to classify transactions like “office supplies,” “travel,” or “contractor fees.” Most accounting software provides a default chart of accounts tailored to Australian businesses.

2. Choose your bookkeeping method

- Single-entry bookkeeping: Records each transaction once (either income or expense). Simple, but limited.

- Double-entry bookkeeping: Every transaction affects two accounts (e.g., money leaves your bank and enters “office supplies”). More accurate and widely used.

3. Choose your accounting method

- Cash accounting: Income and expenses are recorded when money changes hands.

- Accrual accounting: Transactions are recorded when they occur, even if payment hasn’t been made yet. Required for businesses over $10 million in turnover.

4. Establish a spend management workflow

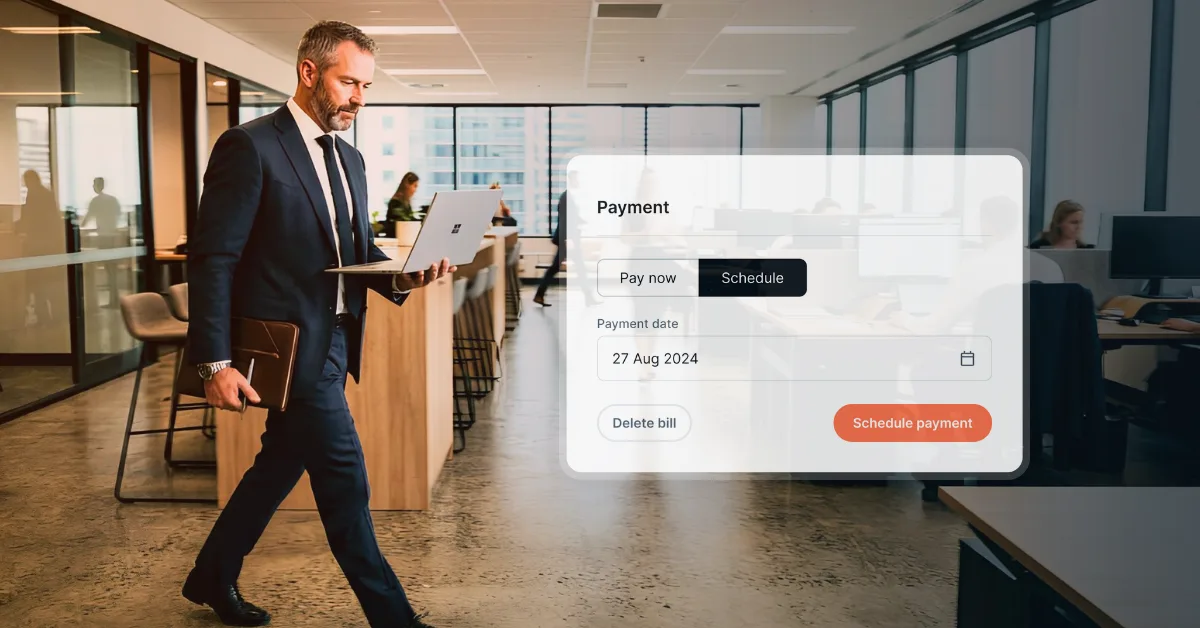

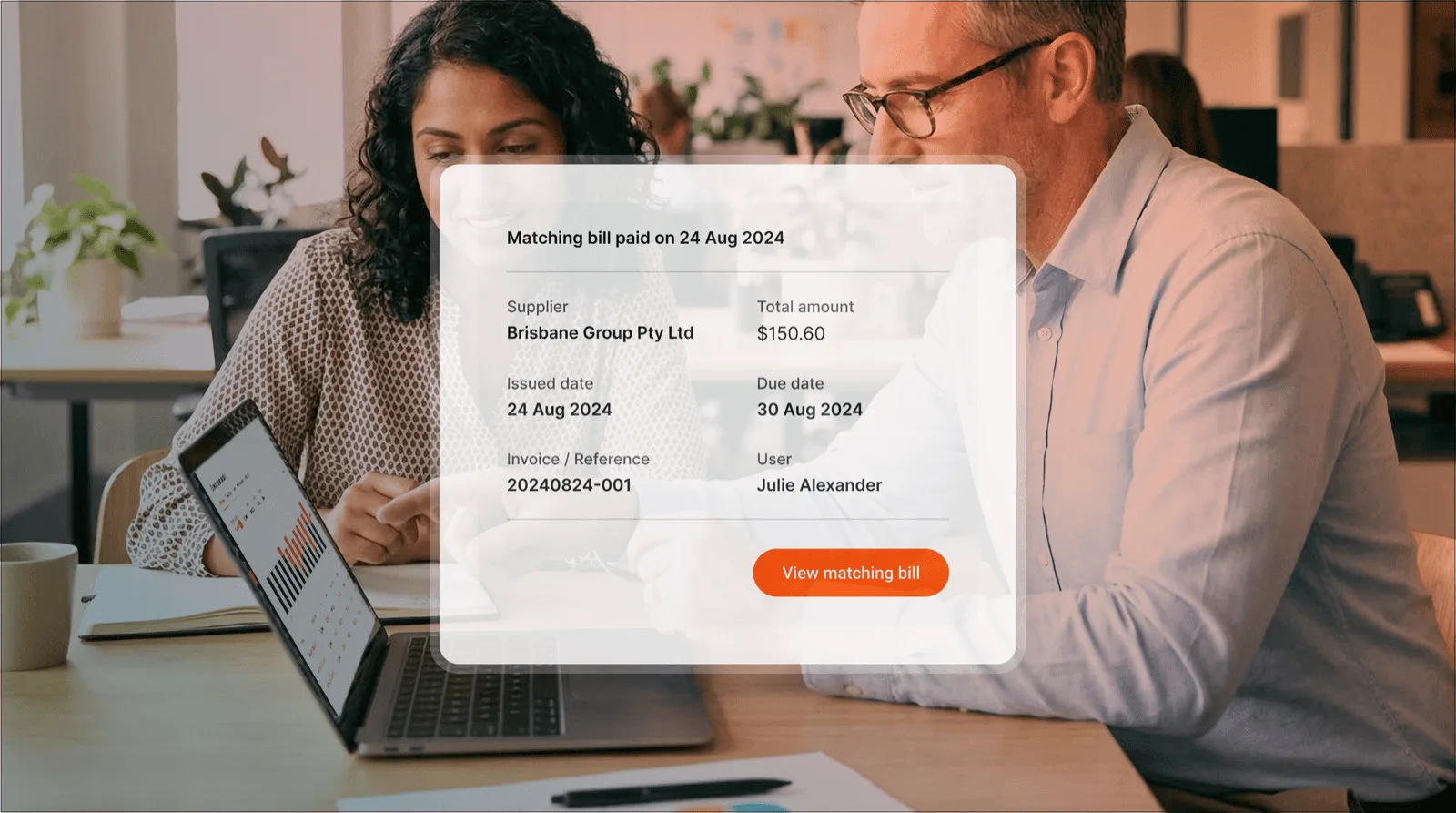

Set rules for how expenses are submitted, approved, and recorded. This is where tools likeBudgetly’s bookkeeper AIassist with categorisation and reconciliation, taking the manual work out of classifying employee purchases.

5. Record transactions

Log every financial event as it happens. The more real-time your data, the better your visibility.

6. Categorise transactions

Assign each transaction to the correct account in your chart of accounts. Miscategorisation can distort reports and cause tax issues.

7. Reconcile regularly

Match your records to your bank statements weekly or monthly. This catches errors early and keeps your data trustworthy.

8. Review reports

Check your profit and loss, balance sheet, and cash flow reports regularly to understand how your business is tracking.

9. Prepare for tax continuously

Don’t wait until June 30. Keep GST records organised, track deductible expenses, and maintain digital copies of receipts throughout the year. Automatic data syncing via Xero integration reduces manual entry and ensures your accounting software is always up to date.

Common mistakes and how to avoid them

Even experienced business owners make these errors. Here’s what to watch for in your business bookkeeping:

1. Not capturing receipts immediately

Receipts fade, get lost, or are forgotten. Use an expense tracking app to capture and store receipts digitally the moment they’re issued.

2. Letting employee spending go untracked

If staff are spending on company cards or being reimbursed, you need a system to track it. Without one, you’ll lose visibility and risk misclassification.

3. Misclassification of expenses

Putting personal expenses in business accounts, or vice versa, creates tax and legal issues. It also makes your financial reports unreliable.

4. No internal spending rules

If there are no limits or approval workflows, overspending and fraud become real risks.

5. Not reconciling frequently

Waiting until the end of the quarter to reconcile makes it harder to spot errors. Weekly or bi-weekly reconciliation is best practice.

6. Mixing personal and business finances

Always keep business transactions separate. Use dedicated business accounts and cards to maintain clear boundaries.

7. Relying on manual spreadsheets for high-volume transactions

Once your business reaches a certain size, spreadsheets become unmanageable. Switching to expense management software reduces errors and saves hours of admin time.

Bookkeeping compliance in Australia

Records required for GST, BAS, and PAYG

If you’re registered for GST, you must keep:

- Tax invoices for purchases over $82.50 (including GST)

- Records of GST collected and paid

- BAS lodgement records

For PAYG and superannuation, keep:

- Payroll records

- Payment summaries

- Super contribution statements

How long to keep records

The ATO requires you to keep most records for five years from the date you lodge your tax return. Some records (like those related to capital gains or depreciating assets) may need to be kept longer.

Acceptable digital storage

Digital records are acceptable, provided they:

- Are a true and clear reproduction of the original

- Are stored securely and can be accessed when needed

- Can’t be easily altered

Cloud-based accounting software and digital receipt storage meet these requirements.

ATO guidelines for small businesses

The ATO provides record-keeping guidance specifically for small businesses. Visit ato.gov.au for the latest compliance information, or speak with a registered tax agent or accountant.

When to outsource your business bookkeeping

Not every business needs a bookkeeper on their payroll. But sometimes, you just can’t keep up anymore. Here’s when you know it’s time to get some help with your bookkeeping:

- Increasing transaction volume: You’re processing too many transactions to manage manually.

- Multiple staff making purchases: Employee spending is hard to track and reconcile.

- Difficult BAS periods: Preparing your BAS has become stressful or time-consuming.

- Growing complexity: You’re dealing with payroll, multiple revenue streams, or inventory.

- Lack of internal expertise: No one on your team has bookkeeping experience or time.

Bringing in outside help doesn’t mean you’re giving up control. Lots of businesses use a mix: they take care of the everyday stuff with tools like Budgetly, then let a professional handle the heavy lifting, things like reconciliation and reports. You still stay on top of things, but it’s a lot less overwhelming.

Better business bookkeeping with Budgetly

Here’s the truth: most business bookkeeping errors start with poor expense management.

When receipts are lost, transactions aren’t categorised, or employee spending isn’t tracked properly, your business’ bookkeeping is already compromised before your bookkeeper even opens the files.

That’s where Budgetly comes in.

Budgetly improves business bookkeeping accuracy from the source by giving you:

- Real-time spend tracking: See what’s being spent, by whom, and on what instantly.

- Digital receipts: Employees upload receipts at the point of purchase, so nothing gets lost.

- Automated categorisation: Transactions are tagged automatically, reducing manual data entry.

- Spending limits and controls: Set budgets and card limits per employee or department.

- Virtual cards: Issue controlled virtual business cards to staff that integrate directly with your accounting system.

- Clean, export-ready data: All your spending data flows into your accounting software in the right format, ready for reconciliation.

By managing expenses properly at the front end, you make your bookkeeper’s job easier and your business bookkeeping reports more accurate. Up to 80% less time is spent on bookkeeping & expense management using Budgetly.

Learn more about how expense management for small and medium businesses can transform your bookkeeping workflow.

Turning bookkeeping data into strategic decisions

Strong bookkeeping gives you more than clean records, it gives you clarity. When your financial data is accurate and up to date, it becomes a practical tool for making better decisions across your business. Clear profit trends show which products or services are actually driving results, while cash flow patterns help you plan ahead, avoid unnecessary pressure, and negotiate better terms with suppliers. Breaking down spending by team or department gives you a clearer view of where money is going and whether it is delivering value, making it easier to allocate resources where they matter most.

With simple systems, digital tools, and consistent habits, bookkeeping becomes quicker and far less stressful. Clean data means fewer errors, easier reporting, and clearer insights, freeing you up to focus on the work that actually drives growth. Good expense management sits at the heart of this, because when transactions are captured and categorised correctly from the start, everything else falls into place.

Budgetly’s Bookkeeper AI helps automate the busywork and gives you instant visibility over spending. Whether you are a sole operator or running a growing team, setting up strong financial habits now will make every decision you make down the line simpler and more informed.