For small business owners in Australia, managing cash flow while building business credit presents a constant challenge. You need credit facilities to grow your business, but traditional lenders often require established credit history that new businesses simply don’t have. Meanwhile, tying up working capital in security deposits feels counterproductive when every dollar should be driving growth.

Most Australian SMEs discover that secured business credit cards, while available overseas, aren’t offered locally. This leaves business owners searching for alternatives that provide credit access without freezing precious working capital or compromising growth opportunities. The problem becomes more frustrating when you realise that traditional expense management approaches create blind spots in spending control, making it harder to demonstrate the financial discipline lenders want to see.

Modern spend management platforms offer a smarter approach. By combining real-time budget controls with automated expense tracking, Australian businesses can build financial credibility while maintaining full access to their working capital for growth investments.

Here’s everything you need to know in under a minute

- Secured business credit cards require cash deposits as collateral but aren’t available in Australia due to responsible lending regulations.

- Instead, Australian SMEs can access better alternatives through modern corporate card platforms and virtual card solutions that provide credit facilities without security deposits.

- These platforms combine automated expense management system capabilities with real-time spending controls, delivering the credit access and financial discipline that secured cards promise without tying up working capital.

- Modern budget management software offers superior financial control for growing Australian businesses.

Table of contents

- What are secured business credit cards

- How secured business credit cards work

- Benefits of secured business credit cards

- Limitations and drawbacks

- Why secured business credit cards aren’t available in Australia

- Best alternatives for Australian SMEs

- How modern spend management replaces secured cards

- Building business credit without security deposits

- Smart expense management for Australian businesses

- How Budgetly delivers better financial control

- Implementation guide for Australian businesses

- FAQs about secured business credit cards in Australia

- The smarter path to business credit control

What are secured business credit cards

A secured business credit card is a type of business credit facility that requires a cash deposit as collateral to establish the credit limit. Unlike prepaid cards, secured credit cards provide actual credit that businesses can use for purchases while building credit history through responsible usage patterns.

The security deposit typically equals the credit limit, so a $5,000 deposit would provide a $5,000 credit line. This deposit remains with the card issuer throughout the relationship and serves as protection against default risk.

Secured business credit cards function identically to regular credit cards for day-to-day operations. Businesses can make purchases up to the credit limit, receive monthly statements, and pay balances over time while incurring interest charges on outstanding amounts.

The key distinction is the upfront collateral requirement, which makes these cards accessible to businesses with limited credit history or poor credit scores that might not qualify for traditional unsecured business credit cards.

How secured business credit cards work

Secured business credit cards operate through a straightforward collateral-based system that reduces risk for lenders while providing credit access to businesses with limited credit history.

The deposit and credit limit relationship

The initial cash deposit directly determines the available credit limit. Most secured cards require deposits between $500 and $25,000, with the credit limit typically matching the deposit amount. Some issuers may offer credit limits slightly below the deposit to account for fees and interest charges.

This deposit remains frozen in a separate account while the card remains active. Businesses cannot access these funds for regular operations or use them to pay monthly balances. The money only becomes available when the account is closed or upgraded to an unsecured card.

Credit building through responsible usage

When businesses use secured credit cards responsibly, the payment history gets reported to major business credit bureaus. Timely payments and low credit utilisation ratios gradually improve the business credit score over time.

This credit building process typically takes 6-12 months of consistent responsible usage before businesses see meaningful improvements in their credit profiles. The key is maintaining low balances relative to the credit limit and never missing payment due dates.

Potential upgrade paths

Many secured card issuers review accounts periodically for upgrade eligibility. After demonstrating responsible payment behaviour for 12-24 months, businesses may qualify for conversion to unsecured cards with deposit refunds.

The upgrade process usually involves a credit review to assess the business’s improved financial position and payment history. Successful upgrades return the security deposit while maintaining or potentially increasing the credit limit.

## Benefits of secured business credit cards

Secured business credit cards offer several advantages for businesses working to establish or rebuild credit history, though these benefits come with important trade-offs.

1. Credit building for new businesses

For startups and businesses without established credit history, secured cards provide an accessible pathway to begin building business credit. Unlike unsecured cards that may require extensive credit history, secured cards are available to most businesses that can provide the required deposit.

The credit building process happens through regular reporting to business credit bureaus including Experian Business, Equifax Small Business, and Dun & Bradstreet. This establishes the business credit profile necessary for future financing opportunities.

2. Employee card capabilities

Most secured business credit cards allow additional employee cards with individual spending limits and controls. This enables better expense management across team members while maintaining oversight of business spending.

Employee cards typically inherit the same security features as the primary card, including fraud protection and purchase dispute capabilities. This provides businesses with better expense tracking compared to employees using personal cards for business purchases.

3. Rewards and benefits programs

Some secured business credit cards offer rewards programs, though typically with lower earning rates compared to unsecured premium cards. Benefits might include cashback on business categories, travel protections, or purchase protection services.

While these rewards are modest compared to unsecured business credit cards, they provide additional value for businesses that must use secured cards to access business credit facilities.

4. Separation of business and personal expenses

Secured business credit cards help maintain proper separation between business and personal finances, which is crucial for accounting accuracy and tax compliance. This separation also protects the limited liability status of corporations and LLCs.

Proper expense separation simplifies bookkeeping, makes tax preparation more straightforward, and provides better visibility into actual business costs and profitability.

Limitations and drawbacks

While secured business credit cards provide credit access for businesses with limited options, they create significant constraints that can hamper business growth and financial flexibility.

Limitation Impact on Business Cost to Business Working capital freeze $5,000-$25,000 tied up in deposits Lost growth opportunities and 0% returns on frozen capital Credit limit caps Cannot exceed deposit amount Restricts purchasing power for larger business expenses High fees and rates 20%+ APR plus annual/monthly fees Increases borrowing costs despite providing collateral Limited rewards Minimal cashback and few benefits Lost opportunity for valuable business rewards and protections Basic functionality No advanced expense management Requires separate systems for budget control and expense tracking

1. Working capital constraints

The most significant drawback is the requirement to freeze working capital as security deposits. For growing businesses, tying up $5,000 or $10,000 in deposits means less money available for inventory, marketing, equipment, or other growth investments.

This capital constraint is particularly problematic for seasonal businesses or those with variable cash flows. The deposited funds remain inaccessible regardless of business needs or opportunities.

2. Limited credit limits

Credit limits are capped at deposit amounts, which may not provide sufficient credit for larger business expenses or growth initiatives. A business needing $20,000 in credit would require a $20,000 cash deposit, effectively doubling the capital requirement.

These artificial limits can constrain business operations and prevent companies from taking advantage of bulk purchasing opportunities or seasonal inventory builds that could improve profitability.

3. Higher costs and fees

Despite requiring collateral, secured cards often carry higher interest rates than unsecured business credit cards. Annual fees, monthly maintenance fees, and employee card fees add to the overall cost of maintaining these credit facilities.

The combination of frozen deposits earning minimal returns and high ongoing fees creates a significant cost of capital for businesses using secured credit cards.

4. Limited rewards and benefits

Rewards programs on secured cards typically offer lower earning rates and fewer bonus categories compared to unsecured business credit cards. Sign-up bonuses are rare, and additional benefits like travel insurance or purchase protection may be limited.

This means businesses sacrifice potential rewards earnings and valuable protections in exchange for credit access, reducing the overall value proposition.

5. Minimal business management tools

Secured cards often lack sophisticated expense management features, reporting capabilities, and integration options that growing businesses need for efficient financial operations.

Without proper expense categorisation, approval workflows, and real-time budget tracking, businesses struggle to maintain tight financial control and visibility into spending patterns.

Why secured business credit cards aren’t available in Australia

Secured business credit cards are not currently offered by Australian financial institutions, leaving local SMEs without this credit building option that’s common in overseas markets.

Responsible lending regulations

Australia’s National Consumer Credit Protection Act 2009 requires lenders to assess applicants’ ability to repay debt based on income and financial situation rather than collateral security. This regulation makes the security deposit aspect of secured cards largely irrelevant to the approval process.

Under these regulations, the cash deposit doesn’t substitute for proper affordability assessments. Lenders must still verify that businesses can service the credit facility through operational cash flows, making secured cards commercially unviable.

Alternative risk assessment approaches

Australian lenders have developed alternative approaches to assess business creditworthiness that don’t rely on security deposits. These include revenue-based assessments, bank statement analysis, and cash flow evaluation methods.

These approaches often provide better outcomes for both lenders and borrowers by focusing on actual business performance rather than available collateral. Modern financial technology enables more sophisticated risk assessment without requiring security deposits.

Regulatory compliance complexity

The regulatory framework around secured credit products in Australia creates compliance complexity that makes these products unattractive for most financial institutions. The cost of regulatory compliance often exceeds the potential profit from secured card products.

This regulatory environment has encouraged innovation in alternative credit assessment methods and business lending products that better serve the Australian market.

Market demand for alternatives

Australian businesses have access to alternative credit building methods through business transaction accounts, bill payments services, and modern spend management platforms that provide similar benefits without requiring security deposits.

These alternatives often provide superior functionality and value compared to secured cards, reducing market demand for traditional secured credit products.

Best alternatives for Australian SMEs

Australian businesses have access to several superior alternatives that provide the credit building and expense management benefits of secured cards without the drawbacks.

Solution Type Credit Access Method Key Benefits Best For Modern corporate cards Revenue and cash flow assessment No deposits, higher limits, real-time controls Growing businesses with steady revenue Virtual card platforms Business performance evaluation Granular control, instant setup, flexible limits Businesses needing departmental spending control Integrated expense management Combined with banking relationships All-in-one platform, automated processing SMEs wanting comprehensive financial management Revenue-based credit Monthly turnover assessment Flexible terms, business-focused Companies with strong sales but limited credit history Business banking facilities Relationship-based assessment Integrated with existing banking Established businesses with bank relationships

1. Modern corporate card solutions

Advanced corporate card platforms assess businesses based on revenue, bank balances, and operational cash flows rather than credit history alone. This enables credit access without security deposits while providing sophisticated spending controls. Learn more about how modern corporate cards work and why they outperform traditional credit products in our guide to corporate cards for Australian businesses.

These platforms often offer higher credit limits than secured cards would provide, with limits based on actual business capacity rather than arbitrary deposit amounts. Real-time spending controls and automated expense management provide better financial oversight than traditional credit cards.

2. Virtual card technology

Virtual card solutions enable businesses to create unique card numbers for different purposes, departments, or projects. Each virtual card can have individual spending limits, merchant restrictions, and approval requirements. Explore how virtual debit cards can provide instant spending controls and enhanced security for Australian SMEs.

This approach provides granular expense control that surpasses secured cards while maintaining full access to working capital. Businesses can instantly create, modify, or cancel virtual cards as needed without affecting other payment methods.

3. Integrated expense management platforms

Comprehensive expense management system solutions combine payment capabilities with automated expense tracking, receipt management, and real-time reporting. These platforms eliminate the manual administration associated with traditional expense management.

Advanced features include automatic transaction categorisation, policy-based approval workflows, and integration with accounting software. This provides the expense visibility and control that businesses seek from secured cards with superior functionality.

4. Revenue-based credit facilities

Alternative lenders in Australia offer credit facilities based on business revenue and cash flow rather than credit history or security deposits. These facilities often provide more flexible terms and higher limits than secured cards.

Revenue-based assessment considers actual business performance rather than historical credit metrics, making these facilities more accessible for growing businesses with strong operations but limited credit history.

5. Business transaction accounts with credit facilities

Many Australian banks offer business transaction accounts with attached credit facilities or overdraft protection. These provide credit access based on account performance and regular banking relationship rather than security deposits.

These facilities often integrate better with existing banking relationships and provide more flexible access to credit compared to separate secured card products.

How modern spend management replaces secured cards

Modern spend management platforms deliver the primary benefits businesses seek from secured cards while eliminating the constraints and drawbacks that limit business growth.

Real-time budget controls vs post-spend reporting

Traditional secured cards provide credit access but limited spending control beyond the credit limit. Modern platforms enforce budget limits, spending policies, and approval requirements before transactions are processed.

This proactive control approach prevents budget overruns and unauthorised spending rather than simply reporting on issues after they occur. Businesses gain the financial discipline benefits of secured cards with superior control capabilities.

Automated expense categorisation and tracking

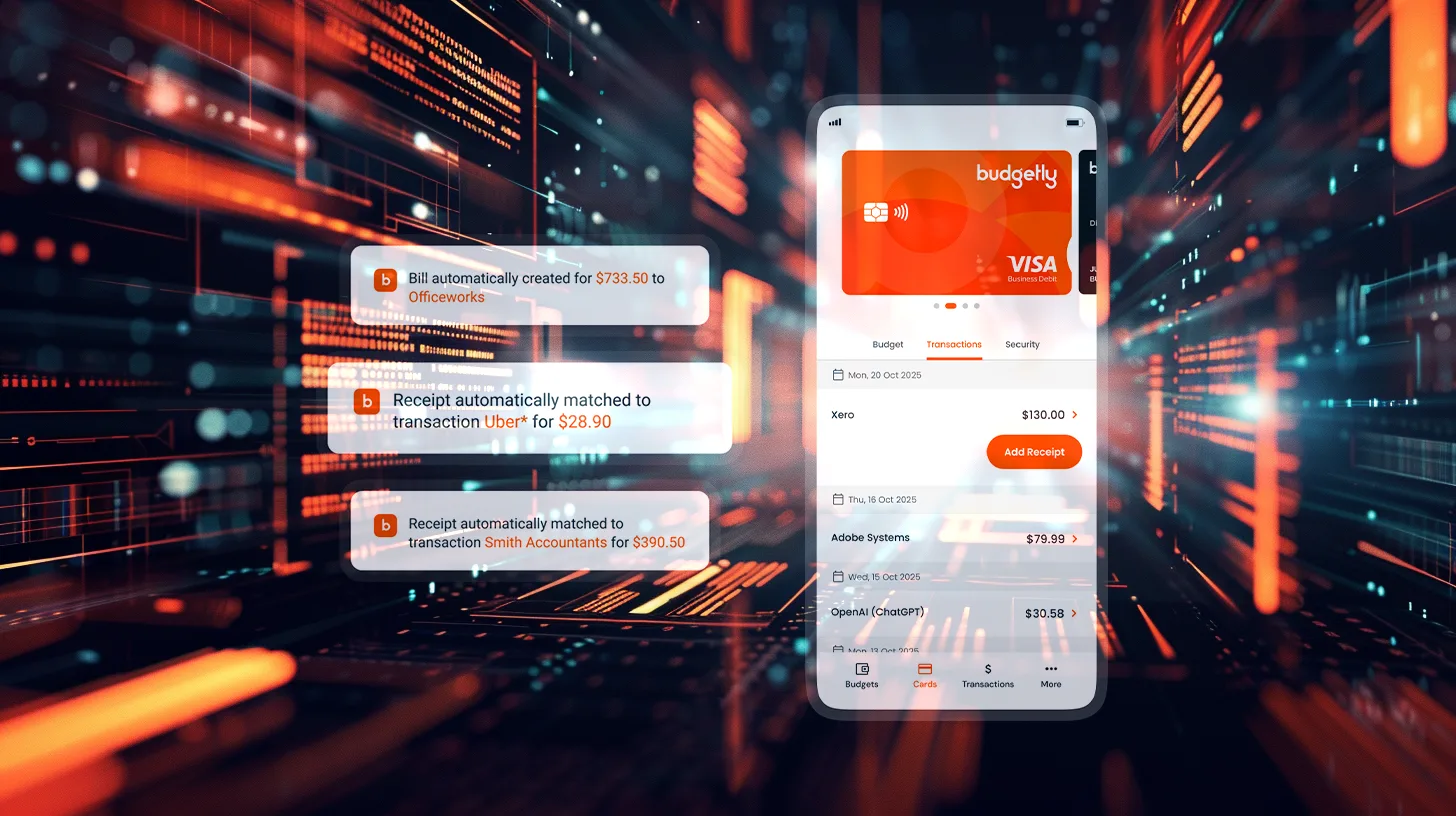

Advanced AI-powered systems automatically categorise business expenses and track spending against budgets in real-time. This eliminates the manual expense tracking that secured card users must handle separately.

Expense tracker functionality includes receipt capture, automatic matching, and policy compliance checking. The result is comprehensive expense visibility without additional administrative burden.

Integration with accounting systems

Modern platforms provide seamless Xero integration and connections to other Australian accounting systems. This eliminates manual data entry and reconciliation work that secured card users typically face.

Automated accounting integration ensures accurate financial records while reducing the administrative time required to maintain proper books. This integration capability is rarely available with traditional secured credit cards.

Working capital preservation

By accessing credit based on business performance rather than security deposits, modern platforms preserve working capital for growth investments. Businesses maintain full access to cash reserves while gaining comprehensive expense management capabilities.

This approach aligns with smart financial management principles where capital should be deployed for maximum business return rather than frozen in low-yield security deposits.

Scalable credit facilities

Modern platforms can adjust credit limits based on business growth and changing needs without requiring additional security deposits. This scalability supports business expansion without artificial credit constraints.

As businesses demonstrate consistent performance and growth, credit facilities can expand accordingly. This eliminates the need to continually increase security deposits to access higher credit limits.

Building business credit without security deposits

Australian businesses can establish strong business credit profiles through strategic use of modern financial tools and disciplined financial management practices.

Establishing business banking relationships

Strong business banking relationships form the foundation of business creditworthiness in Australia. Regular banking activity, maintained account balances, and professional banking relationships demonstrate financial stability to potential creditors.

Business transaction accounts with regular activity create banking history that lenders value more highly than security deposits. This relationship-based approach aligns with Australian banking practices and regulatory requirements.

Consistent payment performance tracking

Modern spend management platforms create detailed payment performance records that demonstrate financial discipline to future lenders. Consistent on-time payments for all business obligations build credibility over time.

These platforms provide comprehensive audit trails and performance metrics that secured cards cannot match. The detailed spending and payment data becomes valuable when applying for additional credit facilities.

Supplier and vendor relationship management

Establishing trade credit relationships with suppliers and vendors creates business credit history without requiring security deposits. Many suppliers report payment performance to business credit agencies.

Professional bill payments management ensures consistent vendor payment performance while maintaining detailed records of all business relationships and transactions.

Financial reporting and transparency

Regular financial reporting and transparent business operations build credibility with potential lenders. Modern platforms provide comprehensive financial reporting that demonstrates business health and management competence.

This transparency approach often carries more weight with Australian lenders than the simple risk mitigation that security deposits provide. Lenders prefer businesses that demonstrate strong financial management over those that simply offer collateral.

Professional financial management demonstration

Sophisticated expense management and budget control systems demonstrate professional financial management capabilities that impress potential lenders. Businesses using advanced financial tools signal competence and discipline.

This professional approach to financial management often results in better credit terms and higher limits than secured cards could provide. Australian lenders value management competence highly in their credit assessment processes.

Smart expense management for Australian businesses

Modern expense management approaches deliver superior results compared to traditional secured credit cards while supporting business growth objectives. For practical tips on improving budget discipline, see our business budgeting guide for Australian SMEs.

Automated receipt and expense processing

Advanced systems capture receipts automatically through email forwarding, mobile apps, or direct merchant integrations. AI-powered categorisation eliminates manual expense coding and ensures accurate financial records.

This automation reduces administrative burden while providing better expense visibility than secured cards with separate expense tracking requirements. Businesses save time while gaining superior financial control.

Real-time spending visibility and controls

Modern platforms provide instant spending visibility across all departments and expense categories. Real-time alerts notify managers of unusual spending or budget threshold breaches before they become problems.

This immediate visibility surpasses the delayed reporting typical of secured card programs. Businesses can address spending issues immediately rather than discovering problems during monthly reconciliation processes.

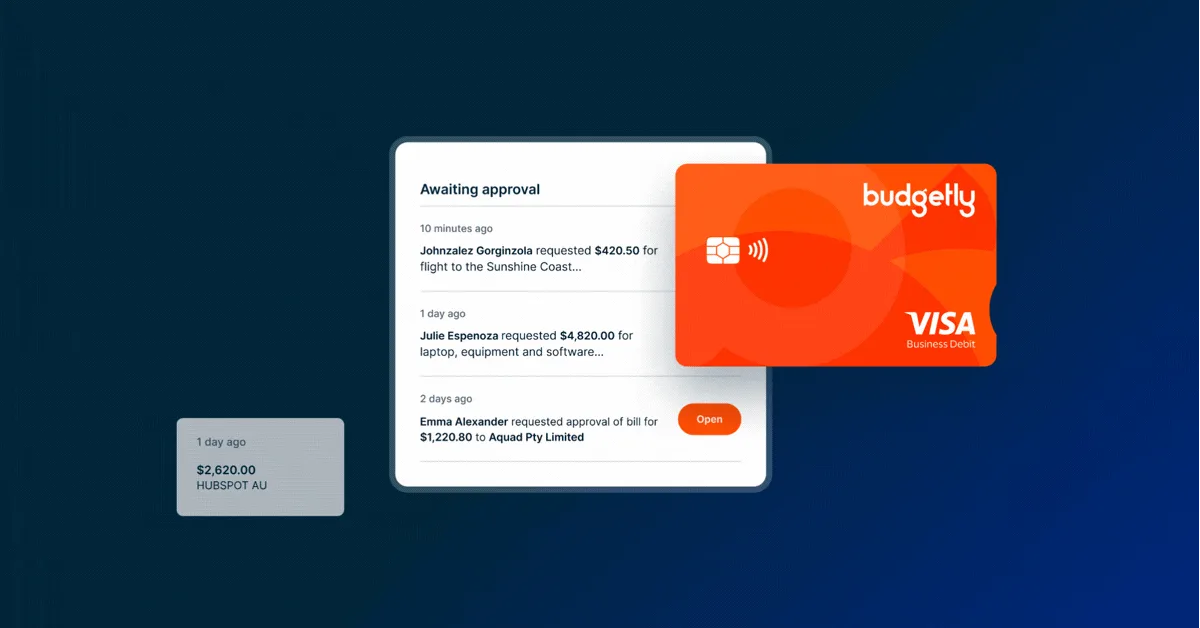

Policy-based approval workflows

Sophisticated approval systems can route expenses based on amount, category, department, or custom business rules. Routine expenses get approved automatically while unusual purchases receive appropriate oversight.

These workflow capabilities provide better spending control than secured cards with basic credit limits. Businesses can implement nuanced spending policies that support operational efficiency while maintaining financial discipline.

Integration with Australian accounting systems

Native integration with Xero and other popular Australian accounting systems eliminates manual data entry and reconciliation work. Financial data flows automatically from expense capture through to final reporting.

This integration capability is essential for Australian businesses but rarely available with international secured card providers. Local solutions understand Australian accounting practices and GST requirements.

Comprehensive financial reporting

Modern platforms generate detailed spending reports, budget performance analysis, and cash flow forecasting. These reports provide insights that help businesses make better financial decisions and demonstrate competence to potential lenders.

The reporting capabilities far exceed what secured cards can provide, giving businesses the financial intelligence needed for smart growth decisions.

How Budgetly delivers better financial control

Budgetly’s AI-first approach to spend management specifically addresses the challenges that lead Australian businesses to consider secured credit cards while delivering superior outcomes.

Feature Traditional Secured Cards Budgetly’s Approach Credit assessment Security deposit required Revenue and performance based Working capital Frozen in deposits Preserved for business growth Expense management Manual tracking required AI-powered automation Budget controls Basic credit limits only Real-time departmental and project controls Reporting Basic monthly statements Comprehensive real-time insights Integration Limited accounting links Native Australian accounting integration Scalability Requires additional deposits Automatic limit adjustments based on performance

AI-powered expense automation

AI bookkeeping & accounting software capabilities automatically categorise transactions, detect policy violations, and identify cost-saving opportunities. This automation eliminates manual expense processing while improving accuracy and compliance.

The AI assistant learns business spending patterns and provides intelligent insights about budget performance, unusual transactions, and optimisation opportunities. This level of sophistication is impossible with traditional secured card approaches.

Real-time budget enforcement

Unlike secured cards that only limit total spending, Budgetly enforces departmental budgets, project limits, and category restrictions in real-time. Spending rules are actively enforced rather than simply reported after the fact.

This proactive approach prevents budget overruns and unauthorised spending before they occur. Businesses gain the financial discipline benefits they seek from secured cards with much better control capabilities.

Comprehensive Australian integration

Native integration with Australian banking systems, Xero accounting, and local payment networks ensures seamless operations for Australian businesses. The platform understands local business requirements and regulatory compliance needs.

These local integrations provide better functionality than international secured card providers can offer. Australian businesses benefit from solutions designed specifically for local market conditions.

Working capital optimisation

By providing credit facilities based on business performance rather than security deposits, Budgetly preserves working capital for growth investments while delivering superior expense management capabilities.

This approach aligns with smart financial management principles where every dollar should work to drive business growth rather than sit idle as security collateral.

Scalable growth support

The platform grows with business needs, automatically adjusting credit facilities and expanding capabilities as businesses demonstrate consistent performance. This scalability supports long-term growth without artificial constraints.

As businesses expand, the platform provides increasingly sophisticated financial management tools while maintaining simplicity for day-to-day operations.

Implementation guide for Australian businesses

Successfully transitioning from considering secured credit cards to implementing modern spend management requires a structured approach that minimises disruption while maximising benefits.

1. Assessing current expense management processes

Begin by documenting existing expense management workflows, identifying pain points, and quantifying the time spent on manual processes. This assessment provides baseline metrics for measuring improvement after implementation.

Common pain points include receipt collection delays, manual expense coding, approval bottlenecks, and reconciliation errors. Understanding these issues helps prioritise which automation features will deliver the most immediate value.

2. Selecting appropriate features and controls

Start with core functionality including automated expense capture, basic approval workflows, and budget tracking. Advanced features can be added progressively as teams become comfortable with the system.

Focus initially on automating the highest-volume, most routine transactions. This delivers immediate time savings while building confidence in the automated systems before tackling more complex expense scenarios.

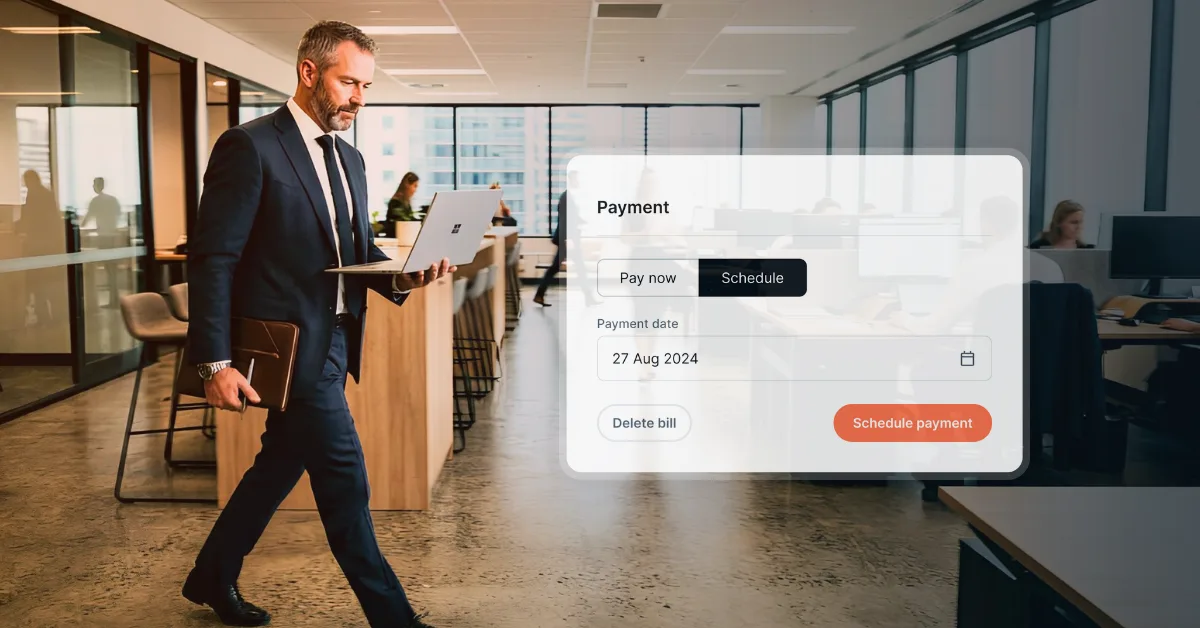

3. Setting up budget controls and approval workflows

Design simple, clear spending policies that cover the majority of business transactions. Complex approval hierarchies can be added later once the basic system is working smoothly.

Effective initial rules might include automatic approval for routine office supplies under $200, manager approval for travel expenses, and director approval for equipment purchases over $1,000.

4. Training staff on new processes

Provide practical training focused on daily workflows rather than technical system details. Staff need to understand how the new processes benefit both their individual work and overall business operations.

Effective training includes hands-on practice with real expense scenarios and clear documentation of policy changes. Regular check-ins during the first month help identify and resolve adoption issues quickly.

5. Monitoring and optimising performance

Schedule regular reviews of system performance, user adoption, and process efficiency. Monthly reviews during the first quarter help identify optimisation opportunities and ensure the system meets business needs.

Key metrics include expense processing time, approval delays, policy violations, and user satisfaction. These metrics guide continuous improvement and demonstrate the value of moving beyond secured credit card limitations.

6. Scaling capabilities over time

As teams become comfortable with basic functionality, gradually introduce advanced features like detailed reporting, integration with project management systems, and sophisticated budget controls.

This phased approach ensures sustainable adoption while building towards comprehensive financial management capabilities that far exceed what secured credit cards could provide.

FAQs about secured business credit cards in Australia

Are secured business credit cards available in Australia?

What alternatives do Australian businesses have instead of secured credit cards?

How can Australian businesses build credit without security deposits?

Do modern spend management platforms work better than secured credit cards?

How long does it take to implement modern expense management systems?

Are virtual cards secure for business use?

What integration options exist for Australian accounting systems?

How do AI-powered expense systems improve accuracy?

AI systems automatically categorise transactions, detect policy violations, identify duplicate expenses, and flag unusual spending patterns. This reduces errors while providing better financial visibility than manual processes or basic credit card statements.

The smarter path to business credit control

The search for secured business credit cards often reflects deeper challenges around expense visibility, spending control, and working capital management that modern solutions address more effectively.

Rather than tying up valuable working capital in security deposits, Australian SMEs can access sophisticated financial management tools that provide better credit facilities, superior expense control, and comprehensive business insights.

The businesses that thrive will be those that embrace proactive financial management rather than accepting the constraints of traditional credit products. Modern spend management platforms deliver the financial discipline and credit access that businesses need while preserving capital for growth investments.

For Australian business owners ready to move beyond the limitations of secured credit approaches and gain real-time control over business spending, explore how comprehensive expense management platforms can transform your financial operations while supporting sustainable growth.